Understanding the Types of Student Loans

7 min read

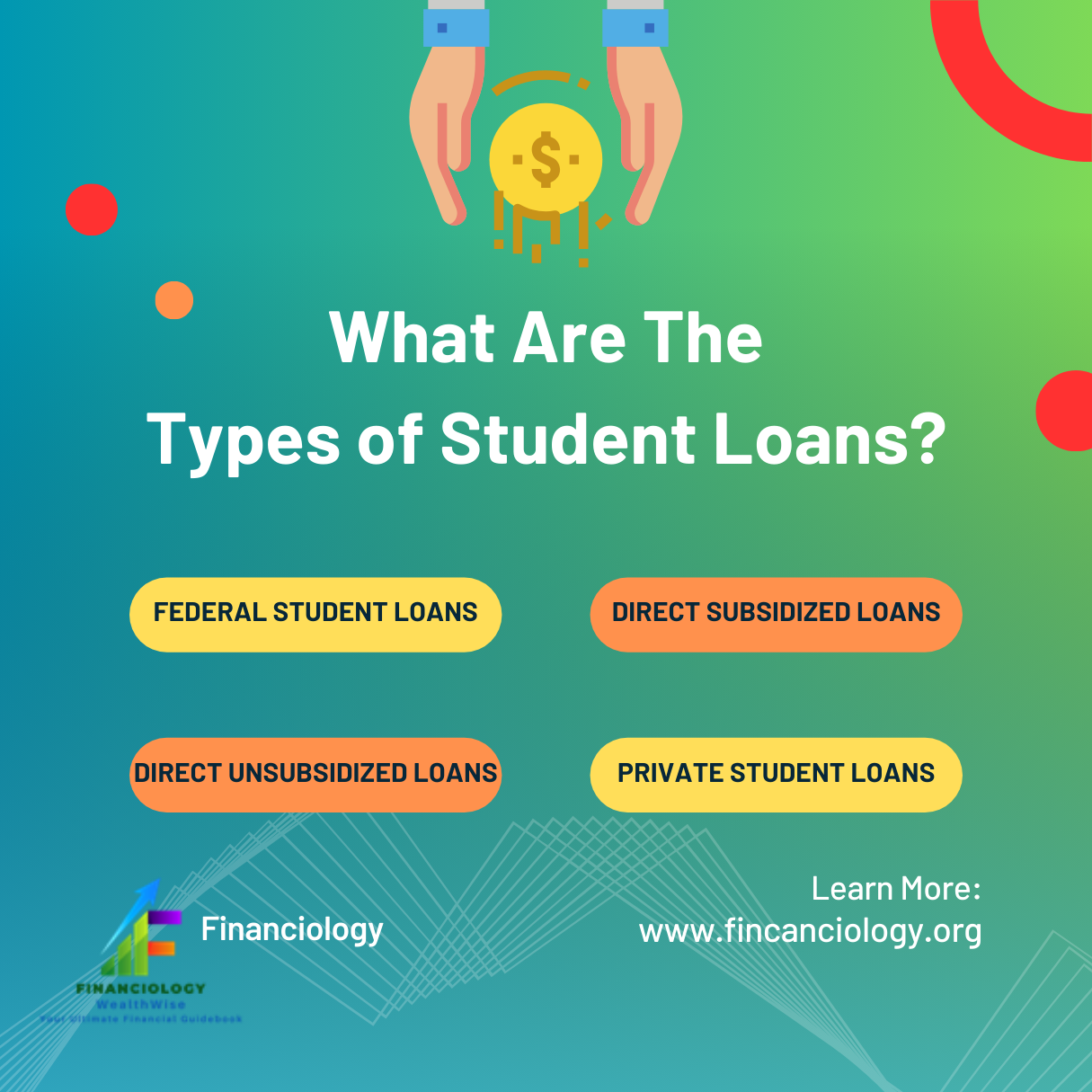

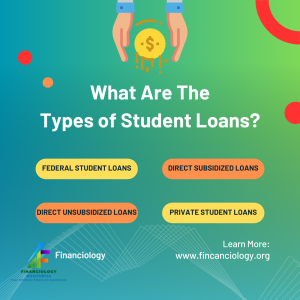

Types of Student Loans

Navigating the Maze:

Understanding the Types of Student Loans

Confused about student loans? WealthWise guide breaks down the different types, helping you make informed decisions about financing your education. Are you gearing up for college but feeling overwhelmed by the prospect of financing your education? You’re not alone.

Understanding the types of student loans available is crucial for making informed decisions about your financial future. Let’s navigate through the maze together and shed light on the various options:

- Federal Student Loans: These loans are funded by the government and typically offer lower interest rates and more flexible repayment options compared to private loans. Subsidized loans are based on financial need, with the government covering interest while you’re in school, while unsubsidized loans accrue interest from the time they’re disbursed.

- Direct Subsidized Loans: Available to undergraduate students with demonstrated financial need, these loans offer the benefit of interest being paid by the government while you’re in school at least half-time, during the grace period, and deferment.

- Direct Unsubsidized Loans: Unlike subsidized loans, these loans are available to both undergraduate and graduate students regardless of financial need. Interest accrues from the time the loan is disbursed, and borrowers are responsible for all interest payments.

- Direct PLUS Loans: These loans are available to graduate or professional students and parents of dependent undergraduate students to help cover education expenses not covered by other financial aid. PLUS loans require a credit check and may have higher interest rates compared to other federal loans.

- Private Student Loans: Offered by banks, credit unions, and other financial institutions, private student loans can fill the gap when federal aid and scholarships aren’t enough to cover educational expenses. However, they often come with higher interest rates and may require a credit check or a co-signer.

- Consolidation Loans: If you have multiple federal student loans, consolidation allows you to combine them into a single loan with a fixed interest rate and a single monthly payment. While this can simplify repayment, it’s essential to weigh the pros and cons, as you may lose certain benefits associated with the original loans.

- Student Loan Refinancing: Refinancing involves taking out a new loan to pay off existing student loans, often with a private lender. This can be a smart move if you can secure a lower interest rate or better loan terms, potentially saving you money over the life of the loan.

Understanding the types of student loans available is the first step toward making sound financial decisions for your education.

Remember to explore all options, compare interest rates and repayment terms, and consider your long-term financial goals before borrowing. With careful planning and informed choices, you can embark on your educational journey with confidence.

Unlocking Opportunities:

How to Qualify for Student Loans?

Ready to finance your education? Learn the essential steps to qualify for student loans and pave the way toward achieving your academic dreams.

Securing funding for higher education can seem daunting, but understanding how to qualify for student loans can make the process more manageable. Whether you’re pursuing undergraduate studies or furthering your education with graduate school, here’s a comprehensive guide to help you navigate the qualification process:

- Fill Out the FAFSA: The Free Application for Federal Student Aid (FAFSA) is the cornerstone of financial aid for college. Completing the FAFSA is the first step in qualifying for federal student loans, grants, and work-study programs. Be sure to gather necessary documents, such as tax returns and income information, and submit your FAFSA as early as possible to maximize your aid eligibility.

- Demonstrate Financial Need: Some federal student loans, such as Direct Subsidized Loans, are awarded based on financial need. To qualify, you’ll need to demonstrate that you require financial assistance to cover the costs of your education. The FAFSA considers factors such as family income, household size, and the number of family members attending college.

- Maintain Satisfactory Academic Progress: Many student loans, both federal and private, require borrowers to maintain satisfactory academic progress (SAP) to remain eligible for funding. This typically includes meeting minimum GPA requirements and completing a certain number of credit hours each semester. Failure to meet SAP standards could jeopardize your loan eligibility.

- Explore Scholarships and Grants: While loans can provide valuable financial support, they also come with repayment obligations. Before taking out loans, explore scholarship and grant opportunities that don’t require repayment. Scholarships are often awarded based on academic achievement, extracurricular involvement, or specific criteria such as ethnicity or intended field of study.

- Consider Federal Work-Study: Federal Work-Study is a federally-funded program that provides part-time employment opportunities for eligible students to help cover educational expenses. Participating in work-study can not only provide financial assistance but also valuable work experience related to your field of study.

- Build a Strong Credit History: While federal student loans don’t typically require a credit check, private student loans often do. Building a positive credit history by making timely payments on existing debts and avoiding excessive debt can improve your chances of qualifying for private loans or securing better interest rates.

- Explore Co-Signer Options: If you cannot qualify for private student loans on your own due to limited credit history or income, consider applying with a creditworthy co-signer. A co-signer with a strong credit history can increase your chances of approval and may help you secure more favorable loan terms.

By following these steps and being proactive in your financial planning, you can increase your chances of qualifying for student loans and access the funding you need to pursue your educational goals.

Explore all available options, compare loan terms, and borrow responsibly to minimize debt burden upon graduation. With careful preparation and informed decision-making, you can embark on your academic journey with confidence.

Related Posts:

How much do student loans give you?

Unlocking Your Educational Potential: Understanding Student Loan Limits!

How much financial aid can you receive through student loans? Learn about the borrowing limits and factors determining how much you can borrow to finance your education.

One of the most pressing questions for students navigating the college financing process is, “How much do student loans give you?” The answer depends on various factors, including the type of loan, your educational level, and your financial need.

Let’s delve into the details to help you understand how much financial aid you can access through student loans:

- Federal Student Loan Limits: Federal student loans, administered by the U.S. Department of Education, have specific borrowing limits depending on the type of loan and your academic status. For undergraduate students, annual loan limits typically range from $5,500 to $12,500, with aggregate (lifetime) limits varying between $31,000 and $57,500, depending on factors such as dependency status and whether your parents qualify for Direct PLUS Loans.

- Graduate and Professional Student Loan Limits: Graduate and professional students may qualify for higher annual and aggregate loan limits compared to undergraduate students. Direct Unsubsidized Loans for graduate and professional students have higher annual limits, ranging from $20,500 to $40,500, with aggregate limits up to $138,500, including any federal loans borrowed for undergraduate studies.

- Financial Need and Cost of Attendance: The amount of student aid you receive is also influenced by your financial need and the cost of attendance (COA) at your chosen institution. Financial need is determined by subtracting your Expected Family Contribution (EFC) from the COA. Your school’s financial aid office uses this information to determine the types and amounts of aid you’re eligible to receive, including grants, scholarships, and loans.

- Dependent vs. Independent Status: Dependent students (those who are claimed as dependents on their parents’ tax returns) may have lower annual loan limits compared to independent students. However, independent students, including graduate and professional students, may qualify for higher loan limits due to their independent status.

- Aggregate Loan Limits: Federal student loans have aggregate (lifetime) limits that cap the total amount you can borrow throughout your education. Exceeding these limits may require exploring alternative financing options, such as private student loans or scholarships.

- Consider Other Sources of Funding: While student loans can provide valuable financial assistance, they should be used judiciously to avoid excessive debt. Explore other sources of funding, such as scholarships, grants, work-study programs, and personal savings, to help minimize reliance on loans and reduce the overall cost of your education.

Recent Posts:

Legal Rights and Responsibilities

Understanding the borrowing limits and factors that influence how much student aid you can receive is essential for making informed decisions about financing your education. Be sure to work closely with your school’s financial aid office to explore all available options and develop a comprehensive plan that aligns with your academic and financial goals.

By leveraging a combination of resources, you can access the financial aid you need to unlock your educational potential and pursue your dreams.